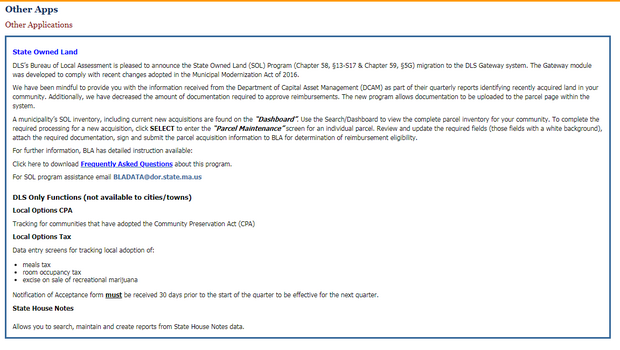

DLS’s Bureau of Local Assessment is pleased to announce the State Owned Land (SOL) Program (Chapter 58, S13-S17 and Chapter 59, S5G) migration to the DLS Gateway system. The Gateway module was developed to comply with recent changes as adopted in the Municipal Modernization Act of 2016.

The Bureau and DLS IT has made every effort to provide you, the system user, with an easy and transparent database program. Gateway will allow you to view old and new records, as well as communicate with the bureau on documentation through an upload and submit process. We welcome your feedback as we go forward with the 2020 launch.

As you may be aware, the Municipal Modernization Act changed the SOL valuation methodology to a statutory formula. This formula utilizes each community’s 2017 valuation and a per-acre valuation derived from that valuation. The “base year valuation” for each city and town was applied for the FY2019 SOL PILOT.

Starting for Fiscal Year 2020, the SOL PILOTS “base year valuation” will require updates annually to include the value of any acquisitions (additional acreage purchased by the state) and/or dispositions (acreage sold, surplus, or transferred to a non-reimbursable agency). For FY 2020, and every two years thereafter, the “valuation” and “per acre valuation” will be adjusted by applying an equalized valuation (EQV) factor.

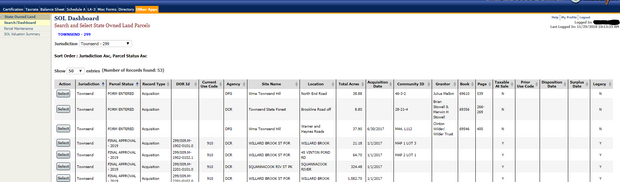

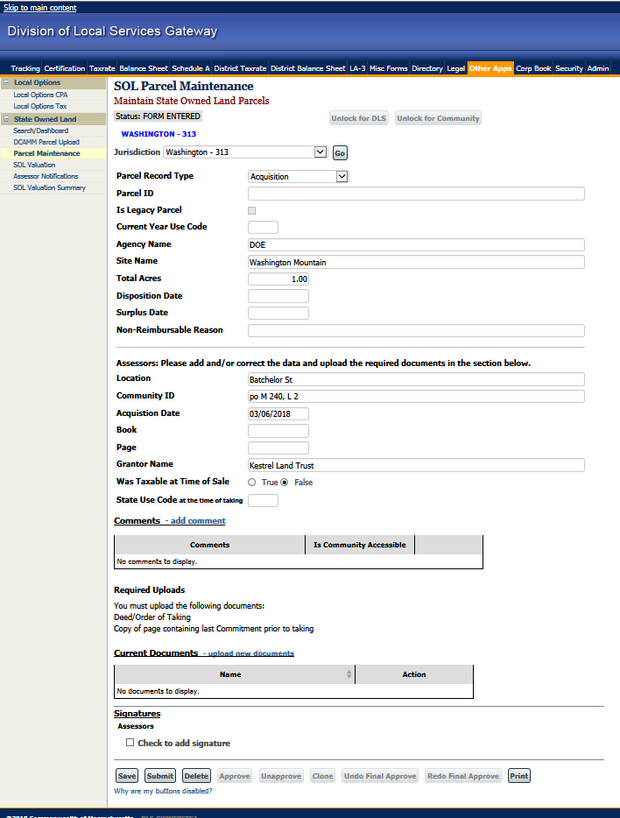

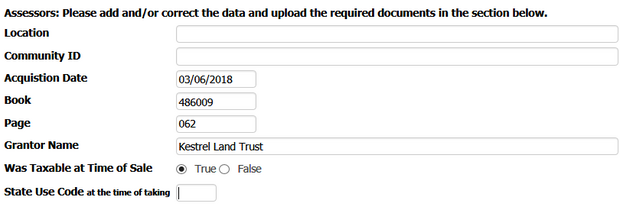

We have received from the Department of Capital Asset Management (DCAM) as part of their quarterly reports recently acquired land in your community. Additionally, we have decreased the amount of documentation required to determine eligibility for reimbursement. The new program also allows documentation to be uploaded to the parcel page within the system.

Under the new law, in preparation for the FY2020 valuation numbers, all newly reported acquisitions from calendar 2017 & 2018 will to be uploaded to Gateway by DLS for processing by March 1, 2019. It is imperative each community respond to the request for information within 30 days. This will insure that the additional acreage will be included in your FY2020 payment.

The criterion for reimbursement eligibility remains the same and is dependent upon three factors:

- taxable status at the time of its acquisition;

- land use;

- and the state agency owning or holding the land.