Withholding on non-exempt members.

If withholding is required, the pass-through entity must:

- Register for pass-through entity withholding

- Make quarterly payments of amounts withheld, and

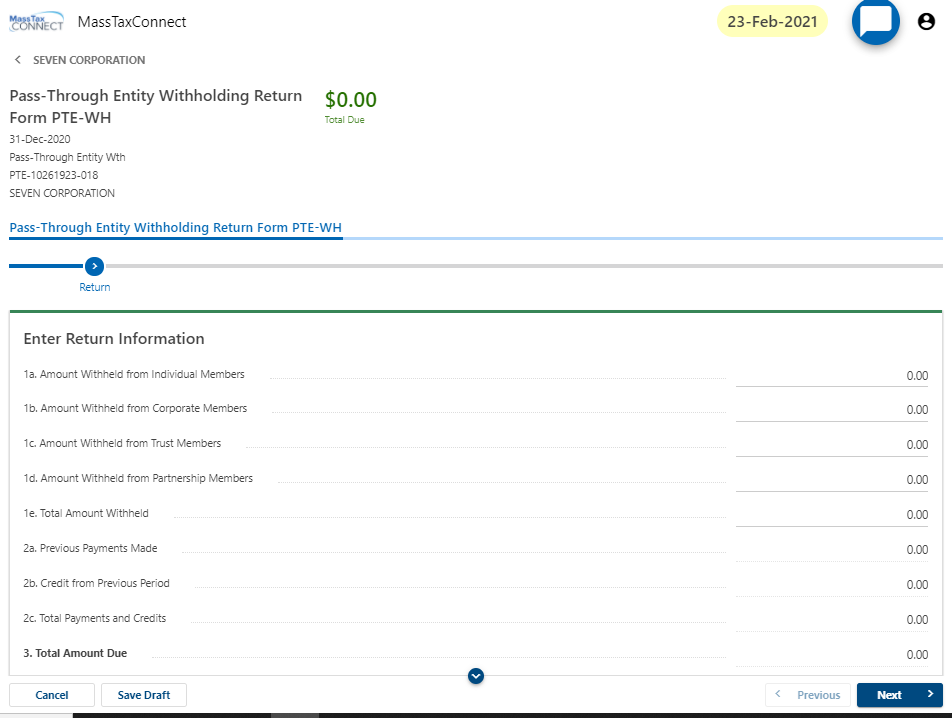

- File an annual withholding return, Form PTE-WH, with DOR.

All of the above must be done online through MassTaxConnect. Form PTE-WH is due March 31st for calendar year filers and must be filed to reconcile previous payments even if no payment is due.

Withholding Amounts

Pass-through entities are required to withhold an amount that is calculated based on Massachusetts taxable amounts of distributive share allocated to a member subject to withholding. The amount subject to withholding is calculated based on the entity’s Massachusetts-source income. The entity must notify each member of the amount withheld or paid on the member's behalf on the Schedule 2K-1, Schedule 3K-1, or Schedule SK-1, as appropriate.

Apportionment

Pass-through entities with income from sources both within Massachusetts and elsewhere must allocate and apportion the income to determine the proper withholding amount, according to the provisions of the Pass-Through Entity Withholding Regulation, 830 CMR 62B.2.2. For non-resident taxpayers who are subject to tax under the personal income tax provisions of M.G.L. c. 62, pass-through entities are required to apportion according to the rules in the Non-Resident Income Tax regulation, 830 CMR 62.5A.1. With respect to corporate partners, pass-through entities should apply the apportionment rules in the Apportionment of Income regulation, 830 CMR 63.38.1.

Determining Withholding Amount; Safe Harbor

A pass-through entity must make an annual payment on behalf of each member subject to withholding. The amount of payment due is determined by multiplying the withholding rate by the lesser of

- 80% of each member's distributive share for the taxable year, or

- 100% of each member's prior year distributive share.

This calculation provides the entity's minimum withholding "safe harbor." The withholding rate for individuals, estates or trusts is the tax rate imposed on Part B taxable income. If the member is a pass-through entity, the withholding entity should use the individual tax rate for Part B taxable income.

The withholding rate for corporations is the applicable tax rate under chapter 63.

The total paid by the pass-through entity is the sum of the tax on the annual allocation of the distributive share made on behalf of each member subject to withholding. A pass-through entity required to withhold that doesn't meet its withholding obligation is subject to the penalties under Chapter 62B and Chapter 62C.

In calculating the amount to withhold, the pass-through entity will apply a single withholding rate to the member's distributive share for the taxable year. For example, the withholding rate for individuals and pass-through entity members is the tax rate imposed on Part B taxable income, even though some of the distributive share may ultimately be subject to a different rate of tax.

The following can be netted in determining distributive share:

- Income

- Gain

- Loss

- Deductions and

- Credits, including a qualified member’s credit for his or her share of the pass-through entity excise paid by the pass-through entity.

Amounts withheld may not be sufficient to meet the individual's estimated payment obligation. As a result, the individual may be required to make estimated payments to ensure that sufficient amounts have been timely paid.

The annual obligation is paid in four quarterly installment payments of 25% of the total amount. Each quarterly payment is due on or before the last day of the month following the close of the quarter of the entity's taxable year.

All payments must be made using ACH Debit on MassTaxConnect.

After the taxable year ends, the withholding pass-through entity will electronically file a "Pass-Through Entity Annual Withholding Tax Return," on or before the last day of the third month of the year following the close of the entity's taxable year, showing the total amount withheld for the taxable year. All non-exempt pass-through entities must file this return, even if no tax was withheld; in such cases the pass-through entity will report zero tax withheld on the form.