Author: Tony Rassias - Deputy Director of Accounts

This article will review municipal enterprise fund data submitted to the Division of Local Services (DLS) Bureau of Accounts (BOA) focusing on current fund types, an explanation of budgeted costs and revenues and fiscal year results of operation. The enterprise fund statute, G.L. c. 44, § 53F½, initially enacted in 1986, gives cities and towns the flexibility to account separately for all financial activities associated with a broad range of municipal services. To learn more details about enterprise funds including reasons why to adopt one, what governmental services are eligible, and how their costs and revenues are budgeted, review the BOA enterprise fund manual.

In FY2026, 276 Massachusetts cities and towns reported 669 enterprise funds led by nine in Barnstable, seven in Beverly and Nantucket, and six in Ashland, Brockton, Westborough and Winthrop. The following table details fund types and number of funds within that reported type. It shows that water and sewer are by far the most common type of enterprise fund.

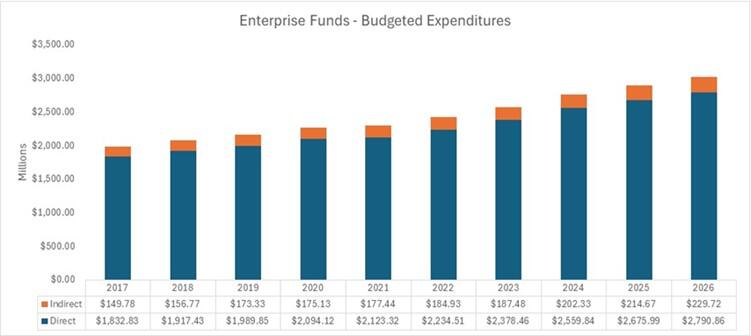

Enterprise budgeted costs are reported on tax rate recap form A-2 as:

- Direct costs, appropriated directly into the enterprise budget

- Indirect costs, appropriated within another fund, most often the general fund, for departmental services to the enterprise and then allocated to the enterprise fund

As shown in the graph below, for FY2026 appropriated direct and indirect costs reported as part of the tax rate certification purposes totaled $3.02B, with $2.79B (92.4%) direct and $229.7M (7.6%) indirect. It also shows how these enterprise funds have grown 52.5% since FY2017 ($1.98B vs. $3.02B). Lastly, it shows that indirect costs as a percent of the total have remained relatively consistent.

The following graph highlights types of direct and indirect costs. It shows that salaries are by far the largest component every year, comprising close to two-thirds of expenses.

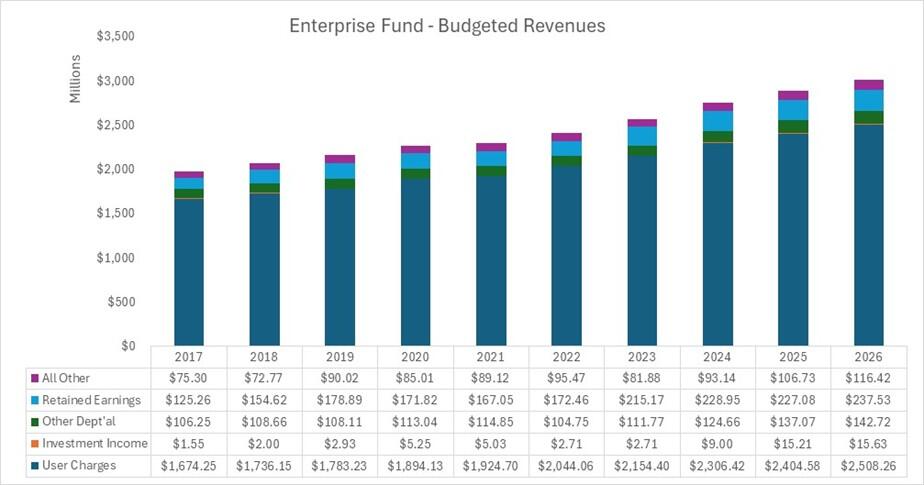

Enterprise budgeted revenues must annually balance with enterprise budgeted costs before a tax rate can be certified by BOA. Costs may be covered by several revenue sources as shown in the graph below. It's important to note that while budgeted revenues must be equal to budgeted costs, enterprise funds do not need to be 100% self-supporting: a municipality can choose to have general fund subsidy. As displayed, the largest source of revenue for enterprise funds is user charges/fees, annually comprising more than 80% of revenue.

The Importance of User Charges and Fees

Since user charges/fees paid by those who use the service (including late charges, fees and interest incurred in the collection process) are the largest source of revenue, it's important that they be estimated prudently. If over-estimated, they could greatly affect retained earnings unless spending is curtailed to offset the shortfall.

Each year as part of the property tax rate setting process, municipalities must provide support of estimated revenues that are above prior year actual receipts by either, or both, (1) a voted rate increase made prior to the submission of the tax rate recap or (2) documentation justifying an increase in usage. The enterprise fund user charge template is used to justify the estimate.

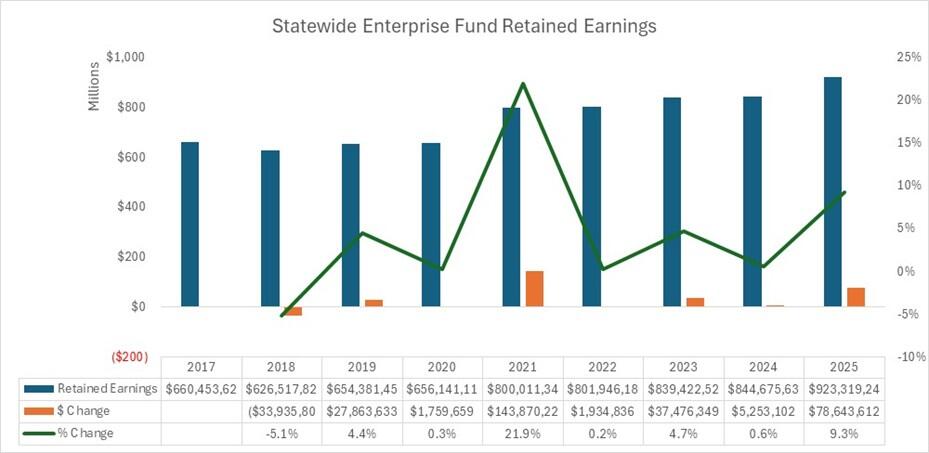

Enterprise retained earnings are similar to free cash in the General Fund. They:

- must first be certified by BOA

- may be appropriated by the community’s legislative body until June 30

- return to $0 as of July 1, and

- cannot be appropriated greater than the amount certified

- have restrictions as found in the enterprise fund guidance.

Actual revenues greater than budgeted serve as a positive factor in the calculation of retained earnings. When the opposite occurs, it’s a negative factor unless appropriations are curtailed to offset a revenue shortfall. The following table shows total certified retained earnings in recent years as of July 1. Certifications shown below as 2025 are as of July 1, 2025 for 324 communities that have submitted a balance sheet as of the time of this writing.

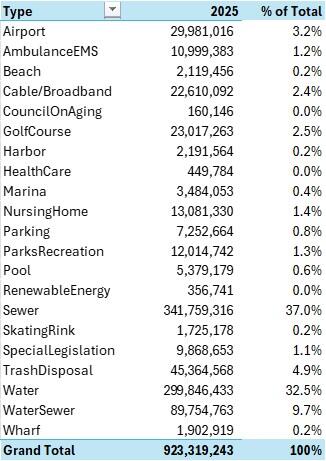

The table below shows the composition of the $923.3M July 1, 2025 retained earnings by enterprise fund type.

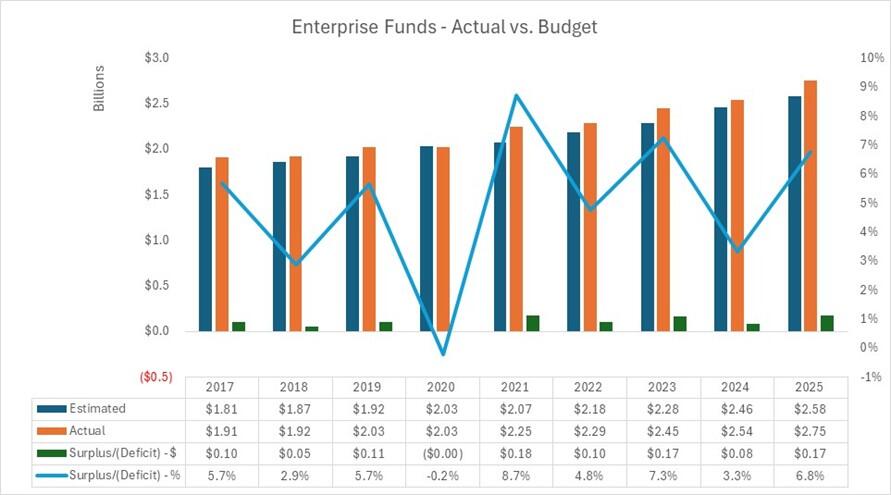

The following graph shows total budgeted estimates to actual revenues submitted to the BOA for tax rate certification purposes since FY2017. (Note: Retained earnings and general fund subsidies are not included in this analysis.)

We hope you found this article informative and useful. DLS has many additional resources related to Enterprise Funds including the Enterprise Fund Manual (IGR-2022-16), Enterprise Fund Best Practices, Trends in Enterprise Funds Data Visualization, Enterprise Funds: Overview and Best Practices (Video) and Completing the Tax Rate Form A-2 for Enterprise Funds Webinar and slides.

Helpful Resources

City & Town is brought to you by:

Editor: Dan Bertrand

Editorial Board: Tracy Callahan, Sean Cronin, Janie Dretler, Jessica Ferry, Brianna Ortiz, Christopher Ketchen, Paula King, Jen McAllister and Tony Rassias

| Date published: | April 2, 2026 |

|---|