Author: Deborah Wagner - Director of Accounts

In a previous City & Town article, we discussed the impact of outstanding receivables on free cash certification. This article expands on that discussion by examining two additional factors that can negatively affect the amount of free cash certified: deficit fund balances (commonly referred to as “hits” to free cash) and overlay.

Undesignated fund balance serves as the starting point for the free cash calculation. The only adjustments required to arrive at free cash should be a deduction for real and personal property tax receivables and an addition for deferred revenue associated with those same taxes. This calculation represents the maximum amount of free cash that may be certified.

However, when a city or town’s balance sheet includes receivables that have not been deferred or reflects deficit fund balances, Division of Local Services (DLS) procedures require that these amounts further reduce undesignated fund balance when determining free cash.

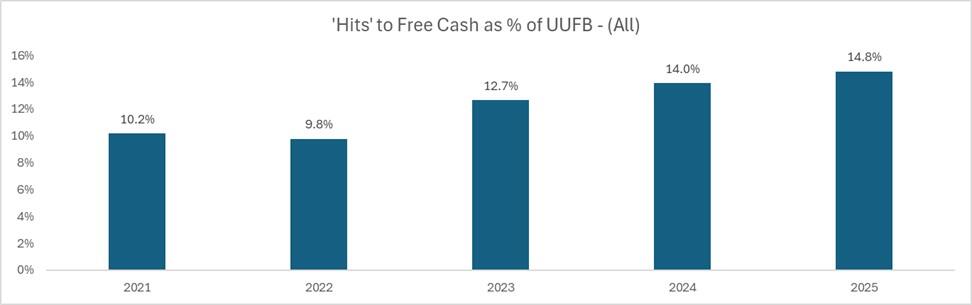

Analysis of balance sheets from 6/30/2021 through 6/30/2025 indicates that “hits” to free cash have steadily increased as a percentage of undesignated fund balance, rising from 10.2% in 2021 to 14.8% in 2025:

The dollar value of these impacts has also grown significantly over the same period. Based on 6/30/2025 balance sheet submissions, free cash certified could have been approximately $583 million higher statewide without the effect of these reductions.

Deficit fund balances that reduce free cash certification most commonly occur in special revenue funds, including grants and revolving funds, as well as capital projects. By law, special revenue funds may not be appropriated, expended, or encumbered beyond available balances. It is the responsibility of departmental personnel and the accountant or auditor to ensure controls are in place to prevent such deficits. Municipalities are strongly encouraged to adopt policies that ensure timely receipt of funds to avoid deficits that negatively impact free cash certification.

In addition, analysis of deferred revenue balances for real and personal property taxes over the same time period shows that, rather than increasing free cash as expected, these balances are often reducing the amount certified.

In 2025, approximately 158 communities reported deferred revenue balances that negatively impacted free cash certification by $172.6 million statewide. This impact was partially offset by municipalities with positive balances totaling $114.4 million, resulting in a net statewide deferred revenue balance of ($58.2 million).

So, what is the relationship between deferred revenue and overlay? When the tax commitment is recorded, real and personal property taxes receivable are debited and deferred revenue is credited in equal amounts. When the annual overlay raised on the tax rate recap is recorded, deferred revenue is debited and overlay is credited, again in equal amounts. Therefore, the following relationship holds true: Real Estate + Personal Property = Overlay + Deferred Revenue.

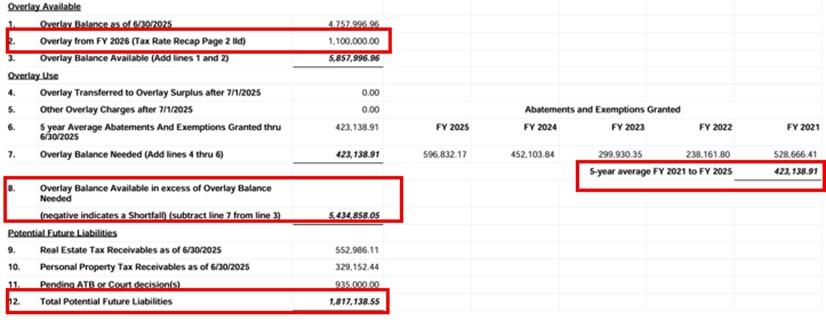

When a municipality consistently raises overlay above the five-year average of abatements and exemptions granted, deferred revenue may eventually become negative, resulting in a reduction to free cash. The below excerpt from the tax rate recap form OL-1 illustrates this point:

Although negative deferred revenue reduces free cash, it may also indicate the presence of excess overlay. In the above example, the difference between lines 8 and 12 would be overlay surplus. This surplus can be released and appropriated for any lawful purpose, provided the Board of Assessors formally votes to do so.

Free cash is a critical financial resource for municipalities. It supports capital planning and provides flexibility to address unforeseen needs. While communities may plan for targeted levels of free cash, a lack of awareness of the factors that can reduce it can undermine those plans.

Please utilize the following DLS resources from our Gateway landing page to understand how your free cash is calculated and how your free cash is generated.

Our Municipal Finance Training and Resource Center also offers information on a variety of municipal finance topics.

Helpful Resources

City & Town is brought to you by:

Editor: Dan Bertrand

Editorial Board: Tracy Callahan, Sean Cronin, Janie Dretler, Jessica Ferry, Brianna Ortiz, Christopher Ketchen, Paula King, Jen McAllister and Tony Rassias

| Date published: | May 21, 2026 |

|---|