Author: Tony Rassias - Deputy Director of Accounts

This article focuses on the municipal Stabilization Fund (Fund), Statewide balance trends, how the Fund is invested and accounted for and how the Fund’s balance can be replenished when depleted. Data is taken from Schedule A, the Annual Report of cities and towns.

Chapter 124 of the Acts of 1945 first authorized Massachusetts cities and towns to appropriate and reserve money as a mechanism to help stabilize the tax rate from the impact of costs “for which the town or city would be authorized to borrow money” under G.L. c.44, §§ 7 and 8 or for another municipal purpose with prior approval of the State’s Emergency Finance Board (EFB). The EFB was created by Chapter 49 of the Acts of 1933, abolished in 2003 and replaced by the Municipal Finance Oversight Board (MFOB) which continues today. Since 1945, several subsequent amendments have been made to G.L. c. 40, § 5B, the Fund’s General Law, eliminating certain requirements and broadening certain restrictions.

There are two fund types. A General Stabilization Fund may be appropriated for any lawful purpose. A Specific Purpose Stabilization Fund may be appropriated for a particular purpose. This type was created by the Municipal Modernization Act, so called, c. 218 of 2016, § 22.

A General Stabilization Fund may be created by a 2/3rds vote of the city, town or district legislative body, requires a majority vote of that body to appropriate into the Fund but a 2/3rds vote to appropriate out of the Fund or transfer from it to another Fund. A Specific Purpose Stabilization Fund may be created by a 2/3rds vote of the city, town or district legislative body, requires a majority vote of that body to appropriate into the Fund and requires only a majority vote to appropriate out of the Fund (a recent change made by Chapter 77 of the Acts of 2023; however there remains a 2/3rds vote to appropriate out of the Fund for a purpose other than for which the Specific Purpose Fund was created.

Either form of Fund may be revoked in the same way it was accepted, subject to charter, but no sooner than three years after acceptance. G.L. c. 4, § 4B. Section 197 of Chapter 77 of the Acts of 2023 also added a special revocation provision for opioid settlement receipts dedicated to a Special Purpose Stabilization Fund, the dedication for which may now be revoked at any time. See Division of Local Services (DLS) guidance on this new provision.

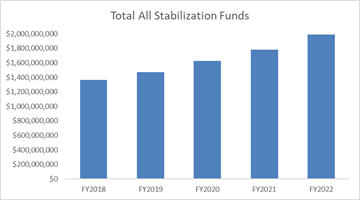

The following graph shows total stabilization fund balances for FY2018 to FY2022 as of June 30 at the time of this writing.

In FY2018, total Stabilization Fund balances was $1.364 billion. In FY2022, the balance grew to $1.987 billion, an increase of 45.7%. The above graph reveals a consistent Statewide trend of annual increases over the five most recent fiscal years. In FY2022, the $1.987 billion consisted of $1.6 billion of General Fund Stabilization and $349 million of Special Purpose Stabilization, as reported by municipalities.

Investing the Fund

As custodian, the treasurer may deposit or invest Fund money into:

- a trust company, co-operative bank, or savings bank

- a national bank, federal savings bank or federal savings and loan association

- the Massachusetts Municipal Depository Trust (MMDT)

- securities that are legal investments for savings banks included in the annual legal list of investments established by the Commissioner of Banks under G.L. c. 167, §§ 15A-15K, and permitted by G.L. c. 167F, § 3 meeting the prudent investment standard governing the investment of public funds in G.L. c. 44, § 55B.

Investment options for this Fund are more liberal than options for other municipal monies but have certain legal restrictions written into the Fund’s General Law.

Accounting for the Fund

All interest earned on the deposit and investment of Fund proceeds belong to the Fund. The treasurer may pool monies from all such funds for investment purposes, but the accounting officer must account for them separately in the general ledger.

For Uniform Massachusetts Accounting System (UMAS) purposes, interest earned as of June 30 on pooled monies are allocated proportionately to each Fund, or if segregated are accounted for within the individual Fund account.

Replenishing the Fund

Fund balance reductions may not be cause for panic if other similar reserves remain healthy. For Special Purpose Stabilization Funds, reductions in fund balance may indicate that the purpose(s) of the Fund has/have been met. For the General Stabilization Fund reductions in fund balance could be an indicator of budget stress. Annual reliance on the General Stabilization Fund is risky, so here are some recommendations on how to maintain a strong balance.

- Don’t Appropriate It All: If you do, the balance will have to be entirely rebuilt.

- Monitor the Fund’s Balance in the Budget Process: Since the Municipal Modernization Act (St. 2016, c. 218) eliminated Fund annual dollar, percentage appropriation and aggregate balance caps, more can be appropriated into the Fund.

- Dedicate an Allowable Revenue Stream into the Fund: By accepting the fourth paragraph of G.L. c. 40, § 5B, a city, town or district legislative body may vote to dedicate a revenue source to a Special Purpose Stabilization Fund by a two-thirds vote. The vote has required language and may include any fee, charge or other receipt except locally assessed taxes, excises and property tax surcharges and revenues reserved by law for particular purposes.

- Vote a Prop 2½ Stabilization Fund Override: Voters may approve a Prop 2½ levy limit override ballot question to fund any Stabilization Fund it establishes. If approved, the additional amount levied is earmarked to that fund in the fiscal year the override is effective and in subsequent years (G.L. c. 59, § 21C(g)

- Adopt a Stabilization Fund Policy: Similar to a free cash policy, adopting a policy on generating and using the Stabilization Fund’s balance is considered a best practice.

For more information on Stabilization Funds, visit the Division of Local Services’ website for further Stabilization Fund guidance.

Helpful Resources

City & Town is brought to you by:

Editor: Dan Bertrand

Editorial Board: Tracy Callahan, Sean Cronin, Janie Dretler, Jessica Ferry, Brianna Ortiz, Christopher Ketchen, Paula King, Jen McAllister and Tony Rassias

| Date published: | December 21, 2023 |

|---|